Here is a sample that showcases why we are one of the world’s leading academic writing firms. This assignment was created by one of our expert academic writers and demonstrated the highest academic quality. Place your order today to achieve academic greatness.

Listed Organisations around the world are required to prepare annual reports presenting their financial condition and disclosures. They are required to raise important issues that are likely to affect the economic decisions of users of financial statements, including investors, shareholders, suppliers management, and government. Part of these overall disclosures is the risk reporting disclosure.

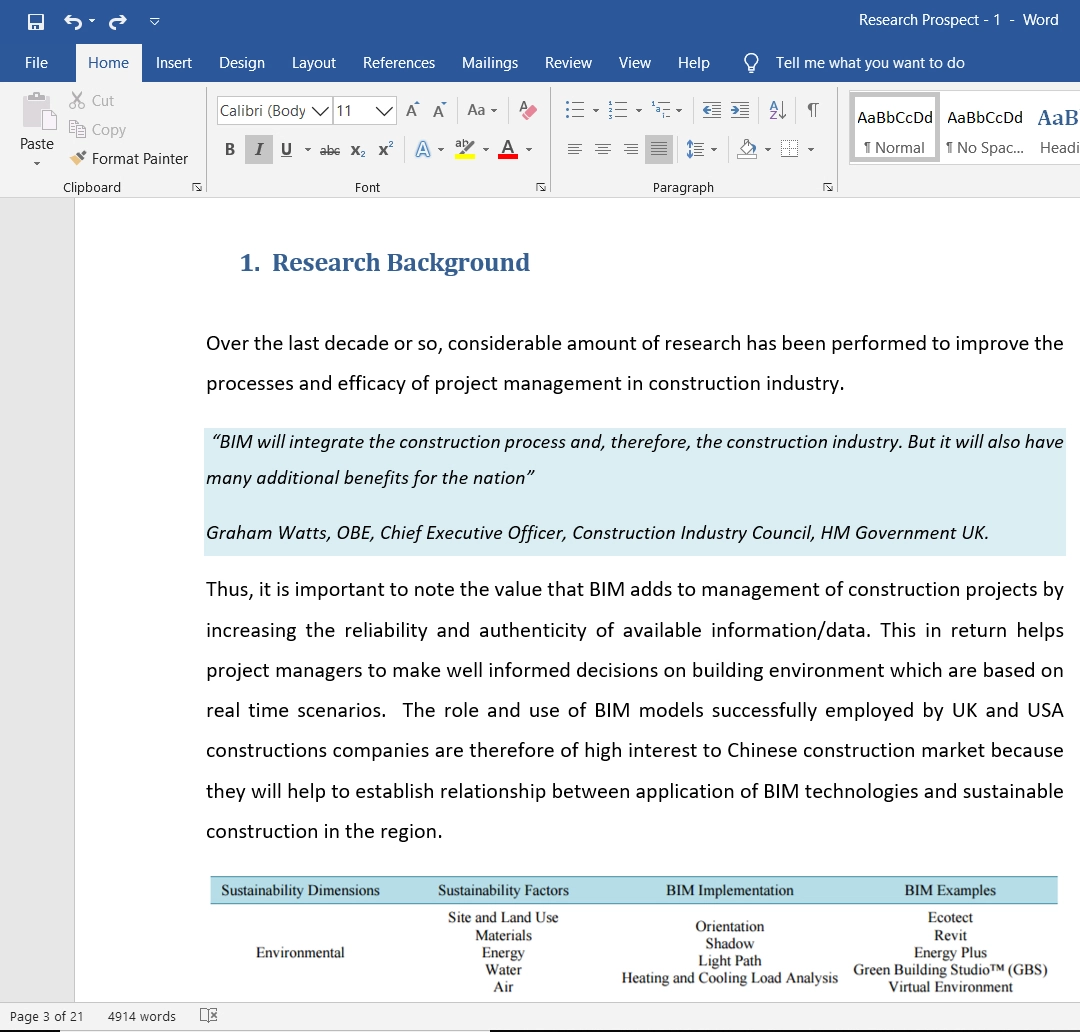

An organization’s risks are required to be reported because every organisation is likely to face risks in achieving its organisational objectives. This essay intends to focus on risk reporting of listed organisations in England and Whales to assess how they disclose risk and why they must improve their risk reporting and how. Based on findings through literature, recommendations have been provided at the end before the conclusion based on new risk reporting principles.

Deumes (2008, p.123) stated that disclosure is an act to release all relevant information of a company that is likely to impact an investment decision. For being listed on Australia’s stock exchange, organisations must follow all disclosure requirements of the Securities and Exchange Commission.

To present a fair view of a company’s financial position, it must include both good and bad information associated with the company. Disclosure items include many perspectives such as the firm’s financial condition, its operating results, and compensation to management and risk disclosures.

This essay is mainly related to risk disclosures that companies must follow so that stakeholders know how much stock of a company is risky to make investment and other decisions. The purpose of presenting risk disclosures is a fair representation of the company’s risk position to base their decision on fair information.

This essay includes seven sections; the first is information disclosed in the annual report by companies, second is associated with risk disclosure in the annual report. The third is different risk perspectives. The fourth represents incentives and disincentives to provide disclosures. The fifth section provides reasons as to why regulators encourage risk disclosure. The sixth gives recommendations to companies for their risk disclosures. Last is the conclusion of the whole essay.

Companies publish an annual report for the use of shareholders to communicate information through it. Directors use this mode of communication to relay vital information about the operations and affairs of the company. It may contain brief information about the vision and mission of the company. Secondly, it includes information on the products and services offered by the company.

Recent developments are mentioned in the report. It displays the strategies, communication from the chairman/CEO, financial review and other business details, risk review and corporate governance requirements, directors’ report, financial statements about the period, auditors report, and additional support information.

The literature about disclosure in the annual report states that shareholders and prospective shareholders use the annual report to aid in their decision-making. In the early days of corporate reporting, the annual report’s information contains only financial information, with details of its financial decisions during the year. Further, in Arshad’s (2011) words, it has been mentioned that current requirements of annual reports have expanded and include a lot of information as listed in the previous paragraph. In addition to this, companies also provide environmental reports and sustainability reports.

These days risk review forms an integral part of the annual report. It explains various kinds of risks faced by the company and measures adopted to address those risks. The shareholders and prospective shareholders are interested in information on business risks faced by the company.

Companies appoint a separate head of risk, sometimes called by the name of the Chief Risk Officer, to assess and evaluate risks faced by the company. The designated person prepares and attaches a separate report called risk review to the annual report as per Abdallah et al. (2015). In the article published by Arshad (2011), risk disclosure is defined as the communication of strategic information and other operational and external information that impacts the company’s progress.

The information included is usually vital for the shareholders’ decision-making. It can be categorized into mandatory information and voluntary information. The article states that non-mandatory information is preferred by the users of the annual reports in making financial decisions and assessing risk exposure.

Risk disclosure in annual reports is affected by certain factors, including the country in which the company is located, the size of the company operating the business, managerial ownership, and the board of directors’ independence. The disclosure requirements are affected by the laws applicable in the country, which define the extent of voluntary disclosure to be made as per Nur Probohudono (2013). The author further states that regulations developed in the UK and US have different effects because of varying regulatory environments. This means that country is a significant factor in determining the level of risk disclosures.

Secondly, as Nur Probohudono (2013) mentioned in the article, the company’s size is also a governing factor in determining the level of risk disclosure in the annual report. The voluntary disclosure depends on the firm size. The fact of whether the company is listed also impacts the quantity of voluntary risk disclosure. It is also mentioned that the responsibilities of companies, larger in size, are high. The same is also said by Elshandidy et al. (2013).

Another factor, as also mentioned in the same article, is the level of managerial ownership. If there are higher hierarchies in the company, risk disclosure is less, and there are fewer chances of communication of risk-related disclosure. The article stated that several studies conclude a negative relationship between the level of management and risk disclosure made by the company. The structure of ownership is a major factor in determining the level of exposure.

Lastly, the board of directors’ independence determines the amount of risk disclosures be made. If the board is not independent and is rather on the company’s payroll, the level of risk disclosures will be high, as mentioned by Khan et al. (2013). Voluntary disclosure needs to be made. In Nur Probohudono’s (2013) article, the studies state that independent directors on the boards emphasize more voluntary information in the annual report.

Orders completed by our expert writers are

Risk reporting is not emphasized by any of the applicable accounting standards in the United Kingdom. The mandatory requirements of disclosure of risk are hence not enforced by any of the regulations. As mentioned in Elshandidy’s (2013) article, some voluntary disclosures are required by the ICAEW.

There are two perspectives of voluntary disclosure of risk information to stakeholders, as per Klumpes et al. (2017). whenever the managers have positive news about the disclosure, they tend to communicate the risk information if it is beneficial as per the cost-benefit analysis. The reason behind more statements disclosed is due to demand from the general public for more transparency. Larger firms are in a better position to disclose information. The mentioned theories presume that one of the largest stakeholders in the disclosure requirement is the shareholder to be met by managers.

Secondly, the banking sector’s risk disclosure perspective is higher than any other sector in the business industry. The banks take huge credit risks in dispersing their lending. As mentioned by Muzahem (2011), there are few risk disclosure theories, one of which, called information asymmetry theory, states that risk disclosure is of great use to investors, analysts,s and other stakeholders of the firm. This disclosure promotes transparency and reduces information asymmetry.

On the other hand, agency theory suggests that relevant information be disclosed, which helps investors ensure compliance with agreements as per the contract. The risk information is disclosed as shareholders pressurize the managers. They appoint high-quality auditors to enable correct information to be presented in the annual report. Some authors state that there are reasons why managers would disclose risk information, as this would disclose that they have risk management systems.

The signaling theory emphasises that directors may want to signal investors’ profitability, hence disclosing risk information to attract better investments. Lastly, there is political cost theory, which means companies disclose risk information to overcome contracting and political costs and pressure generated.

Companies must provide disclosures; however, they hesitate to do so because there are also drawbacks of presenting risk disclosures. After all, they may act against the company. This section of the essay is related to incentives that encourage companies to present risk disclosures and disincentives to doing the same. Following are the incentives and disincentives of presenting risk disclosures in the annual report;

Dobler (2008, p.186) stated that any company and its operations are transparent if it has disclosed all the required information that it is required to tell; however, companies that do not provide complete disclosures can be seen with a wary eye. Stakeholders may think that its risk position may be weak due to which it has not disclosed the information so that stakeholders do not take any decision against the company.

Therefore, companies are encouraged to show all necessary and required information in their annual report to ensure transparency. On the other hand, according to Woods and Humphrey (2008, p.47), companies with strong positions and lower risks are specifically encouraged to present risk disclosure because there is no risk that stakeholders will decide against the company. Further, the company’s position becomes intense on the stock exchange because its share value is enhanced due to transparency.

Additionally, companies receive and retain independent auditors’ trust as they think it responsibly reports what it is required to report. Hence, there is no need for detailed scrutiny. Furthermore, risk disclosure enables management to critically look at its risk position and compare it to the previous year’s risk position to assess whether the risk is enhanced or deteriorated.

Based on which it can design and implement relevant policies. Listed companies in England and Whales are required to follow the requirements of ICAEW in which demand risk disclosures in detail so that transparent information is presented to the stakeholders. This requirement of ICAEW encourages companies to give risk disclosure.

Despite the many benefits of disclosing risk, organisations hesitate to present an absolute position in their stakeholders because of their decisions against the company. According to Elzahar and Hussainey (2012, p.135), if an organisation and its position are at risk, stakeholders will withdraw their stake in the company. Risk disclosures are the most common disincentive because companies try to attract stakeholders through their annual reports rather than disappoint them. Any stakeholder will look for any positive information and prefer to invest in a lower-risk company.

A major goal of a listed company is to attract stakeholders for its benefit. Still, stakeholders look for their benefit and prefer a lower-risk company to secure their funds. Furthermore, high-risk disclosure may compromise its position at the stock exchange, and its shares may go down if the company is highly risky. Moreover, Said Mokhtar and Mellett (2013, p.839) stated that sometimes it may be difficult to measure risk appropriately when the case is complicated yet important; such complication may also discourage the company from reporting risk or the fear that investors will withdraw their investment.

According to the regulators, Ryan (2012, p.297) stated that two primary purposes for risk disclosures are risk assessment and decision making. This decision-making is associated with all stakeholders of the company, including management. Risk assessment is very important for organizations as it enables them to become aware of their actual position. They may generate high profits but are also highly risky due to their capital structure or other issues.

According to Vandemaele and Michiels (2009), Risk reporting has been an issue over which ICAEW did pioneering work between 1997 and 2002. It called that risk reporting should be significantly improved. Since the time, there has been a material expansion in risk reporting and its quality. Regulators say that risk in business is more than the likelihood of corporate failure. There may be unexpected collapses that inevitably require a focus on the quality of risk reporting and may enhance unrealistic expectations.

For instance, risk reporting enables organizations to prevent failures in the future. Even risk reporting is not a guarantee that it will provide reliable early warning regarding any failure. However, risk reporting is necessary because there is always a risk that an organization may fail to achieve its objectives. ICAEW has focused on investors’ benefits by stating that they face various risks on their investment and are willing to face such risks in exchange for higher returns. Because they are eager to take these risks, they deserve to know all uncertainties within an organisation because they have a stake in the company.

If a material risk is not disclosed, they lose their money and may not trust the organisation again. It implies that non-disclosure of risk can be harmful to both organisation and investors or other stakeholders. Rajab and Handley-Schachler (2009, p.226) stated that investors consider business risks so far as they know them. Most investors who are risk-seeking to achieve higher returns should not think that the company will lose its investors by reporting risks.

However, hiding the existence of risk from stakeholders will result in losing their trust, and such an act is more likely to lose stakeholders. This is why regulators encourage companies to disclose risk because it helps gain and retain the trust of stakeholders. According to Hill and Short (2009, p.755), regulators are of the view that risk reporting is a product of the risk appetite of the company determined through the extent and nature of principle risks faced and such risks that a company is willing to take for the achievement of organisational objectives.

Reporting requirements should not drive risk appetite itself. Some executives are likely to suspect that when stakeholders and regulators ask for detailed and robust risk reporting, they ask organisations to take fewer risks. However, there doesn’t need to be a correlation between the sensitivity of company performance, the quality of risk reporting, and the robustness of the process that produces the risk. It implies the importance of risk reporting to companies. Regulators even say that it helps encourage companies to take fewer risks.

Recently, risk reporting has been a noticeable topic for organisations because ICAEW has increased its requirements regarding risk reporting and demands that companies disclose risk transparently (Elshandidy and Hussainey, 2013, p.323). This consideration of ICAEW implies that risk reporting is something significantly crucial for companies and their stakeholders. Two primary purposes of risk reporting, as stated by ICAEW, are risk assessment and decision making.

A company must assess its risk position because there is always some risk in achieving organisational objectives. There are levels and extents of these risks. They may or may not be material. Still, a ban organisation must disclose all material risks that it thinks can impact stakeholders’ decisions. Regulators, professional bodies, and stakeholders expect that organisations report both internally and externally because risk reporting is beneficial for stakeholders and the company itself.

The current requirement to improve risk reporting requires companies to be even more transparent in presenting their position, and regulators believe risk becomes lower when a company reports it correctly. Therefore, it is recommended that all listed companies on the stock exchange of England and Whales shall present risk disclosures appropriately. The improvements required by ICAEW included seven principles through which risk reporting could be improved. They are; companies should tell users what they want to know.

It should focus on quantitative information, integrate into other disclosures, management should think beyond the annual reporting cycle, list of principal risks should be short, current concerns should be highlighted, and report on risk experience (Linsley and Shrives, 2006, p.389). Every organisation listed on England and Whales’s stock exchange must follow these seven principles to make its risk reporting transparent and reliable. Even in the absence of regulatory requirements, external auditors challenge organisations and their executives on these disclosures. Now when regulation requires companies to improve these disclosures, then auditors will be even more cautious. It is recommended that every listed company must keep these seven new principles into consideration while making disclosures.

This essay is associated with risk disclosures and current requirements of risk disclosures by regulators and professional bodies, including ICAEW. The essay focuses on the importance of risk disclosures for the company and its stakeholders by stating that stakeholders base their financing decisions on the annual report and its components. A very integral part of the yearly report is risk disclosure. Risk disclosure is made for risk assessment and decision-making.

Risk assessment is mandatory for organizations to devise policies to bring down the level of risk. A high level of risk shows that the company is likely to suffer loss, resulting in a fall in the company’s share price and ultimately losing its market share and reputation. Therefore, risk must be minimized, and regulators believe that reporting risk appropriately can be a measure to bring down the risk. The essay includes a section in which the effect on risk disclosures is determined. It is found that risk disclosure in annual reports can be affected by country, company size, managerial ownership, and board independence.

This essay also discusses different perspectives of risk and incentives and disincentives of organisations to disclose risk, which says that stakeholder trust is gained and retained through proper risk reporting. Still, the disincentive is that the company fears losing its stakeholders who are not ready to take risks. However, there are risk seekers who are willing to invest in organisations with higher risks. It should be noted that regulators are now giving more importance to risk reporting because it has become necessary for organisations and stakeholders. It requires organisations to follow seven principles mentioned in the previous section associated with risk reporting to make it transparent and reliable so that stakeholders can rely on such disclosures.

Abdallah, A.A.N., Hassan, M.K. and McClelland, P.L., 2015. Islamic financial institutions, corporate governance, and corporate risk disclosure in Gulf Cooperation Council countries. Journal of Multinational Financial Management, 31, pp.63-82.

Arshad, R. and Ismail, R.F., 2011. Discretionary Risks Disclosure: A Management Perspective. Asian Journal of Accounting and Governance, 2, pp.67-77.

Deumes, R., 2008. Corporate risk reporting: A content analysis of narrative risk disclosures in prospectuses. The Journal of Business Communication (1973), 45(2), pp.120-157.

Dobler, M., 2008. Incentives for risk reporting—A discretionary disclosure and cheap talk approach. The International Journal of Accounting, 43(2), pp.184-206.

Elshandidy, T., Fraser, I. and Hussainey, K., 2013. Aggregated, voluntary, and mandatory risk disclosure incentives: Evidence from UK FTSE all-share companies. International Review of Financial Analysis, 30, pp.320-333.

Elshandidy, T., Fraser, I. and Hussainey, K., 2013. Aggregated, voluntary, and mandatory risk disclosure incentives: Evidence from UK FTSE all-share companies. International Review of Financial Analysis, 30, pp.320-333.

Azahar, H. and Hussainey, K., 2012. Determinants of narrative risk disclosures in U.K. interim reports. The Journal of Risk Finance, 13(2), pp.133-147.

Hill, P. and Short, H., 2009. Risk disclosures on the second-tier markets of the London Stock Exchange. Accounting & Finance, 49(4), pp.753-780.

Khan, A., Muttakin, M.B. and Siddiqui, J., 2013. Corporate governance and corporate social responsibility disclosures: Evidence from an emerging economy. Journal of business ethics, 114(2), pp.207-223.

Klumpes, P., Ledlie, C., Fahey, F., Kakar, G. and Styles, S., 2017. Incentives facing UK-listed companies to comply with the risk reporting provisions of the U.K. Corporate Governance Code. British Actuarial Journal, 22(1), pp.127-152.

Linsley, P.M. and Shrives, P.J., 2006. Risk reporting: A study of risk disclosures in the annual reports of U.K. companies. The British Accounting Review, 38(4), pp.387-404.

Muzahem, A., 2011. An empirical analysis of the practice and determinants of risk disclosure in an emerging capital market: United Arab Emirates (Doctoral dissertation, University of Portsmouth).

Nur Probohudono, A., Tower, G. and Rusmin, R., 2013. Risk disclosure during the global financial crisis. Social Responsibility Journal, 9(1), pp.124-137.

Rajab, B. and Handley-Schachner, M., 2009. Corporate risk disclosure by U.K. firms: trends and determinants. World Review of Entrepreneurship, Management, and Sustainable Development, 5(3), 224-243.

Ryan, S.G., 2012. Risk reporting quality: Implications of academic research for financial reporting policy. Accounting and business research, 42(3), pp.295-324.

Said Mokhtar, E. and Mellett, H., 2013. Competition, corporate governance, ownership structure, and risk reporting. Managerial Auditing Journal, 28(9), pp.838-865.

Vandaele, S., Vergauwen, P. and Michiels, A., 2009. Management risk reporting practices and their determinants.

Woods, M., Dowd, K. and Humphrey, C., 2008. The value of risk reporting: a critical analysis of value-at-risk disclosures in the banking sector. International Journal of Financial Services Management, 3(1), pp.45-64.

All work is written by human writers. 100% AI free, guaranteed.

100% money back guarantee if you find plagiarism in our work.

COMPANY DETAILS