Upload your assignment, essay, research paper, or dissertation draft and our academic experts will review it and provide structured feedback within 24–48 hours.

Disclaimer: This is not a sample of our professional work. The paper has been produced by a student. You can view samples of our work here. Opinions, suggestions, recommendations and results in this piece are those of the author and should not be taken as our company views.

Type of Academic Paper – Essay

Academic Subject – Business

Word Count – 3000 words

Executive Summary

Brexit has presented the United Kingdom with numerous uncertainties on various aspects such as the economic and political landscape. As a result, the sterling pound has been on a gradual decline which further weakened the competitiveness of the UK market. Regarding the insurance market, some positive projections are attributed to the increasing rate of employment, which hints at an expected increase in the demand for insurance products and services.

This report presents an analysis of the competitiveness of Prudential U&E in the insurance market. First, it is acknowledged that the company has adopted a holistic approach in marketing and sales by employing third-party financial firms, its own Prudential Financial Planning, and an in-house direct sales team to have a wider market reach. Secondly, the company ensures it gets the best out of its employees by involving them in the management process/ decision-making and nurturing some of their talents to improve their level of performance in service delivery. Lastly, to succeed in the insurance industry, it is pivotal to explore the opportunities presented by big data and social media. So far, Prudential is making efficient use of social media, but it is still yet to harness data gathered through its Enterprise Data Warehouse to gain additional competitive advantage.

Introduction

It is normal practice for any competitive business to evaluate its position within the industry it operates in and self-evaluate to identify its areas of strengths and weakness. In addition, the evaluation is also generally aimed at identifying the opportunities available to the business and threats that could derail its performance or even its survival. Based on the findings from the evaluation, the business is expected to implement recommendations that have been extrapolated to protect its competitive position, increase its profitability, and sustain its operation for the long run (Cagica and Luisa, 2017).

The focus of this paper is to analyse the position of Prudential U&E within the UK insurance industry and even the internal factors of the company that are determinants of its success. In particular, the analysis will focus on Prudential U&E’s business environment and of industry survival and success factors. Secondly, the analysis will look at Prudential U&E’s organisational strategy. Thirdly, the focus will be on the company’s culture, structure, management systems, and human resource strategy. The last section will be based on a critical appraisal of the strategy.

Hire an Expert Writer

Orders completed by our expert writers are

Formally drafted in an academic style

Analysis of the Organisation’s Business Environment and of Industry Survival and Success Factors

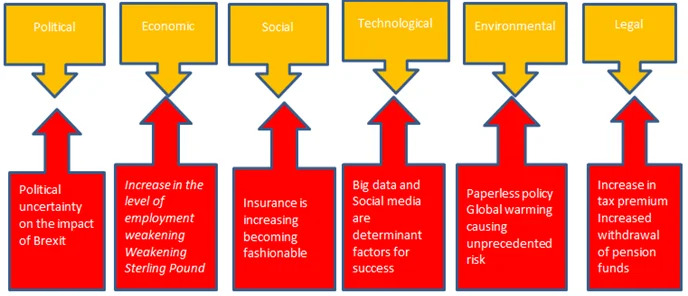

Pestel Analysis

Political: Brexit has brought about changes in the political landscape of the UK vis-à-vis the European Union and there are still uncertainties whether UK will still be a competitive market after the full exit and whether regulations such as Solvency II, which were to be rolled out across all EU-member states, will still take effect in the UK.

Economic: Increased levels of employment guarantee a sustained increase in the uptake of insurance products but the vote of Brexit still bears economic uncertainties, which have started to be demonstrated by the weakening position of the sterling pound.

Social: It is increasingly becoming fashionable to have an insurance cover to be protected against unforeseen eventualities; the paradigm shift of social perspective on insurance business will result in increased uptake of insurance products.

Technological: The past decade has witnessed a revolutionary change in the way technology impacts business operations and profitability. So far, in the insurance industry, there is the increased use of big data in the decision-making process and social media for interactions with customers.

Environmental: most major insurers in the UK have implemented a paperless policy, which has resulted in the industry’s reduction of carbon footprints. The aspect of global warming has presented uncertainty of certain risk covers. For example, areas that were previously not prone to flooding can be ravaged by floods leading to outstanding claims.

Legal: Increase of tax on insurance premium from 6% to 9.5% and expected future increases will mean increased cost of insurance to UK’s households. The loosening of stringent regulations that guard against withdrawal or access of pension savings has elicited increased withdrawal of pension funds and reduced uptake of annuities, which erodes the liquidity of insurance companies, thus limiting their abilities to reinvest premiums.

Pestle Framework

Porter’s Five Forces

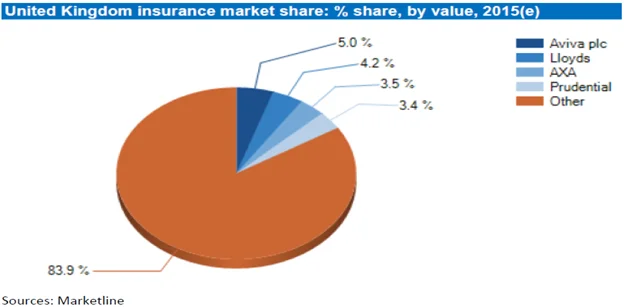

Competition in the Industry: Among the leading competitors in the UK insurance industry include Aviva Plc, Lloyds, AXA, and Prudential. 83.9% of the market share is shared by a pool of other insurance company as shown in the image below. This goes to show the industry is highly populated by small players who have been motivated by low entry requirements, more so from the online platforms. Additionally, facts show that the four leading players command smaller percentages because the industry services are not highly differential, making it hard to gain a unique competitive advantage that can earn them a substantial market share.

UK’s Insurance Market Share

New Entrants into the Industry: in the near future, after the full implementation of the Solvency II rule, it will become harder for new entrants to venture into the industry owing to high capital requirements.

The Power of Suppliers: third-party financial advisers and independent direct sales representatives act as the key suppliers to the insurance industry. They wield a lot of power over the insurance companies owing to their high number, which means they will always go to the highest bidder and this, in essence, drives up the cost of products

The Power of Customers: In the insurance industry, there are two categories of customers. First, those who make bulk purchases and hence issued with a discount are large organisations such as airlines, construction companies, and pharmaceutical companies, among others. The second category comprises individual buyers who contribute a small portion of the insurer’s total sales. Consequently, bulk purchases, i.e. large organisations, are the only ones to wield a high power over insurance companies, but the individual buyers have a weak bargaining position against the insurers.

The Threat of Substitutes: the increased popularity of price comparison websites has equally increased the threat of substitutes. When customers use such websites, they become aware of the many insurers available in the market and even the differential factors across each insurer. Ergo, a slight change in offering could motivate the customer to switch to another insurer.

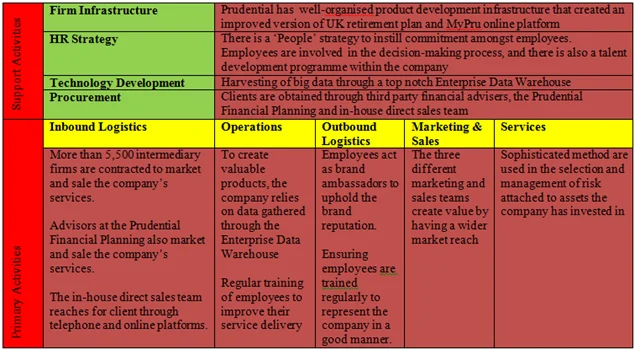

Firm Infrastructure: The Company has a well-organised product development framework through which it can design products that will give it a competitive advantage in the marketplace. For example, recent product development efforts led to the improvement of its UK retirement plans, which were in conformity with the pension reforms that occurred in 2015. The other latest result from product development is the MyPru, an online platform that enables customers to control their products without having to visit the physical branch. This product is also aimed at gaining a competitive advantage through enhancing customer experience.

Technology Development: The Company boasts of a top-notch Enterprise Data Warehouse that harvests data across its entire business network that can be harnessed to create more value through the further development of futurist products that will meet the expectations of evolving customers’ needs.

Human Resource Management: Through the ‘People’ strategy, the company aims at creating a high-performance culture whereby employees input is welcomed in the management process. Regularly, the employees participate in open forums with the senior managers to discuss the company’s performance and such engagement instils a spirit of commitment amongst the employees. Thirdly, to enhance the performance through skills development, the company has implemented a talent development programme and an apprenticeship programme. Lastly, employees are regularly trained on effective working practices to ensure they always deliver their best in assigned tasks/roles.

Procurement: To acquire clients, the company employs the use of third-party financial advisors who have been able to push the sales growth of the insurers by 7% on an annual basis for the past seven years. The company’s subsidiary (Prudential Financial Planning) is also responsible for bringing sales into the company. For example, in the past financial years, it increased its sales by 77%. Lastly, the company also acquires sales through an in-house direct sales team that makes sales pitch via the internet or through telephone calls, albeit the efforts of this team was dismal in the last financial year since the sales were 40% lower compared to the previous year. The different avenues for customer attractions ensure the company has a wider reach across the target market.

Primary Activities

Inbound logistics: The three players in the sales distribution channel are responsible for bringing businesses into the company, and as previously mentioned, they comprise third-party financial advisers, the Prudential Financial Planning, and an in-house direct sales team. Considering a big percentage of sales originate from third-party advisors, the company has ensured it does not rely on a few advisors but rather a pool of 5,500 intermediary firms to protect against unforeseen eventually of a few firms backing out from the contract. The combined efforts of these three sources guarantee the company of increased sales and sustained growth.

Operations: To create value in its operation, the company harness data to its top-notch Enterprise Data Warehouse, this is then used in the development of products that will improve customer experience and the level of satisfaction. The aspect of operations that creates value is the regular training of employees for better service delivery to improve customer experience, thereby making them loyal to the business.

Outbound Logistics: To safeguard its brand reputation, the company needs to ensure those dealing directly with customers are well trained and act effectively as the brand ambassador of the company. Advisors working in the direct in-house sales team and Prudential Financial Planning are under direct supervision from senior managers, and hence their representation of the company is guaranteed. The only existing loophole would have been within the third party financial advisors who operate semi-independently. However, through its representation of 180 staff positioned at the intermediary firms, there is a guarantee that customers are handled accordingly.

Marketing and Sales: By employing a diverse marketing and sales team, the company has been guaranteed a wider market reach. The increased sales reported from the third party financial advisors and advisors at Prudential Financial Planning has affirmed the efficacy of using financial advisors as marketing and sales representatives.

Services: to safeguard the investments made by their customers, the company creates value through its asset share fund whereby it employs a sophisticated method of selection and management of risk for each re-investment it undertakes using funds from the customers.

In conclusion, the value chain analysis of Prudential U&E well demonstrates how it effectively collects premiums and converts to profits through the investments that it makes through an array of activities. Secondly, there are well-orchestrated activities aimed at marketing and selling the company’s products and services through three different sales entities.

Analysis of Prudential U&E’s Culture, Structure, Management Systems, and HR Strategy

The structure of the company is designed in a manner that portrays geographic representation, i.e. the markets where it operates (US, UK, and Asia) and product line representation (asset management and insurance services). Since 2001, the company has integrated all operations to eliminate the duplication of roles and place a greater emphasis on customer needs. Operations integration means that all support activities have been centralised, and devolution is not practised within the organisation structure.

The systems in place depict bureaucracy, which is cognizant of all companies that operate in sectors where product and service delivery needs to be standardised, which require adherence to strict cultural controls to attain the organisational goals. Moreover, employees’ contribution is adopted through a well-guided process, which means they do not have the autonomy to make changes to the company they deem fit.

The company’s culture is based on the belief that both customers and employees ought to be treated with respect, and this shows there is a humanistic approach towards management of people within the company, and each person is valued for the contribution they make towards achieving the organisational goal.

The human resources strategies are aimed at making the employees more efficient. Moreover, the talent development program is aimed at harnessing the skills and capabilities of the employees in a manner that will deliver desired results to both the employee and the organisation.

There are obvious areas of weakness, which hint at inappropriate and biased human resource strategies within the company. For example, the CEO of Prudent U&E had to step down because of a personality clash with the newly recruited CEO of the Group. Thirdly, it acted unfairly in a manner that demonstrates economic disincentive by transferring 81 administrative jobs to India to save £2million per year; nevertheless, the new CEO John Foley hired new senior managers who will equally cost more money to the company. Lastly, the company laid off formal staff only to later recruit 45 apprentices in a move that could be misconstrued as avoiding paying set/expected salaries and employing draconian cost-saving measures.

In conclusion, the company has a good organisational culture that is customer and employee focused. However, there are instances where its HR strategies have contravened the spirit of fairness and respect to its employees.

Critical appraisal of Prudential U&E’s Strategy

Resources & Capabilities

Is it valuable

Is it rare

Is it imitable

Is it non-substitutable

Financial resources

Yes – it accords Prudential the opportunity to invest in the development of new and unique products. Secondly, the company is able to diversify to other markets thus further increasing its profitability.

No – Prudential is ranked fourth vis-à-vis the UK market share. Therefore, the other three leading insurers (Aviva Plc, Lloyds, & AXA) are equally likely to have access to colossal amount of financial resource

Yes – competitors can seek a reinjection of capital to generate massive financial resources

Yes – financial resources are always a prerequisite in product development and market diversification

Brand reputation

Yes – the company has been in operation since the late 19th century. Meaning it is a solid business that can withstand market shocks.

No – Lloyds is 329 years old while AXA is 200 years old and they have more market share than Prudential

Yes – Aviva plc is only 17 years old and it is the market leader.

Yes – brand reputation is critical to the success of an insurance company.

Three levels of marketing and sales

Yes – by selling through intermediary firms, Prudential Financial Planning, and direct in-house sales team the company is able to cover a wider market share

No – other insurers have equally implemented the same selling strategy

Yes – there many insurers who can implement the same strategy

No – the marketing and selling strategy can be re-strategized to be solely done by the company’s in-house marketing team/department or it can be outsourced.

The harnessing of big data to gain a competitive advantage is a critical survival factor in the insurance industry. Considering Prudential, U&E has yet to explore this opportunity fully whilst it already has a well-structured Enterprise Data Warehouse, which means it is putting its market position or competitiveness in jeopardy. The other area where Prudential’s strategy has shortcomings is its HR strategy. Despite aiming at nurturing commitment and improving the skills of its employees, it is still unable to implement fair employment practices, and it even engages in economic disincentives by offshoring some jobs to India.

The UK’s economic and political platforms present numerous uncertainties, although the employment rate has been on an increase and new government regulations make insurance products more convenient for customers. Both of these factors are likely to increase insurance uptake. With the expected increase in entry capital requirement for new entrants, it will mean the already established insurers such as Aviva Plc, Lloyd AXA, and Prudential are set to benefit from the new appetite for insurance products.

In conclusion, the insurance industry has positive performance growth projections, and there is set to be cutthroat competition among existing players as new entrants are likely to be locked out despite the possibility of an increase in insurance products. Ergo, it is critical for Prudential U&E to implement responses that can guarantee its survival and gain success in the industry.

References

Cagica, C., Luisa, 2017. Handbook of Research on Entrepreneurial Development and Innovation Within Smart Cities. IGI Global.

Chen, X., Zhu, S., 2015. DroidJust: Automated Functionality-aware Privacy Leakage Analysis for Android Applications, in: Proceedings of the 8th ACM Conference on Security & Privacy in Wireless and Mobile Networks, WiSec ’15. ACM, New York, NY, USA, p. 5:1–5:12. doi:10.1145/2766498.2766507

(Please drop us an email if you would like to review the complete list of references…)

DMCA / Removal Request

If you are the original writer of this essay and no longer wish to have the essay published on the www.ResearchProspect.com then please: